Contents:

Key Odyssey Network Indicators

Shipper Actions

In today’s competitive environment, becoming a preferred shipper to carriers can help improve attaining sufficient capacity. Things that shippers offer that help reach this status can include:

Accuracy:

-

Forecast for the end of month/end of quarter – plan for surges in your needs to ensure coverage

-

Develop order lead time – at least 5 days in advance. ask carriers for “best case” options

Specificity:

-

Request delivery windows from customers…often 8 a.m. deliveries are requested when product really is not need until much later. A window of 8-10 a.m. may have a better chance of coverage.

-

Spread delivery times across the day

-

Assess what your customers really need. Make sure that customer delivery requirements are up to date and accurate. Do not require equipment/assessorials that are not needed

Flexibility:

- Offer flexible load times

- Explore/ be open to mode options including intermodal

Driver-friendliness:

- Load/unload within the normal 2 hours-time is money to drivers

- Provide creature comforts (clean restrooms, rest areas, free Wi-Fi, a cup of coffee, etc.)

Consistency:

- Offer consistent volume that carriers can plan against

- Reduce order changes – a new date may put coverage at risk

Efficiency:

- Maximize payload on trucks

- Utilize trailer drop yards at high volume origins when possible

- Prioritize loading/unloading trucks quickly at facilities

Promptness:

- Pay carriers within their contracted freight terms- cash flow is vital to carriers

Economic Update

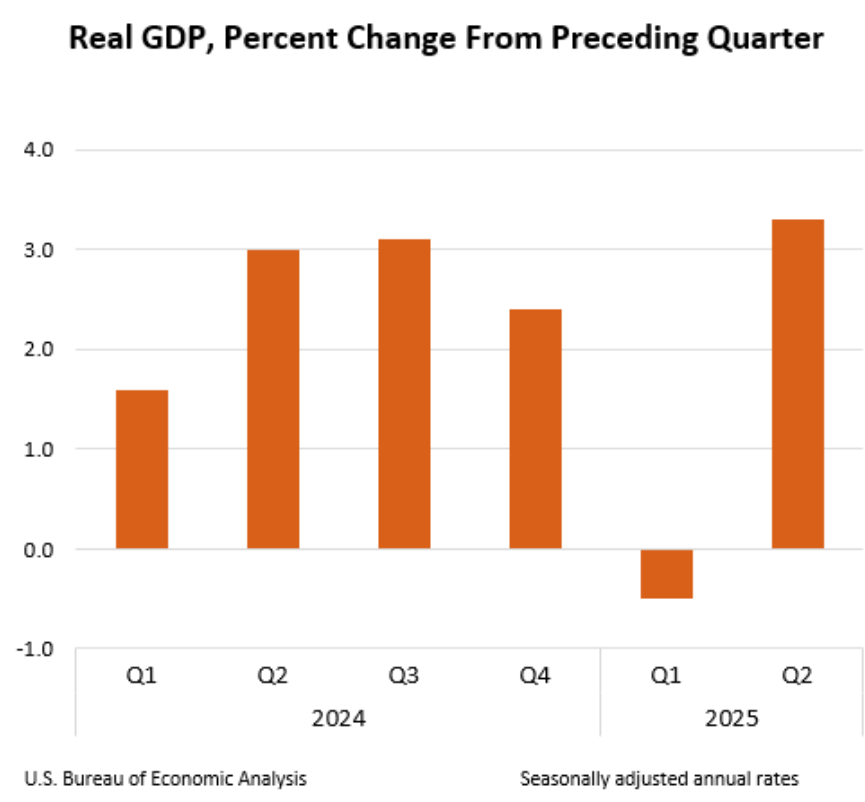

GDP Change

Gross Domestic Product | U.S. Bureau of Economic Analysis (BEA)

- Real gross domestic product (GDP) increased at an annual rate of 3.3 percent in the second quarter of 2025 (April, May, and June), according to the second estimate released by the U.S. Bureau of Economic Analysis. In the first quarter, real GDP decreased 0.5 percent.

- The increase in real GDP in the second quarter primarily reflected a decrease in imports, which are a subtraction in the calculation of GDP, and an increase in consumer spending.

- These movements were partly offset by decreases in investment and exports.

Unemployment

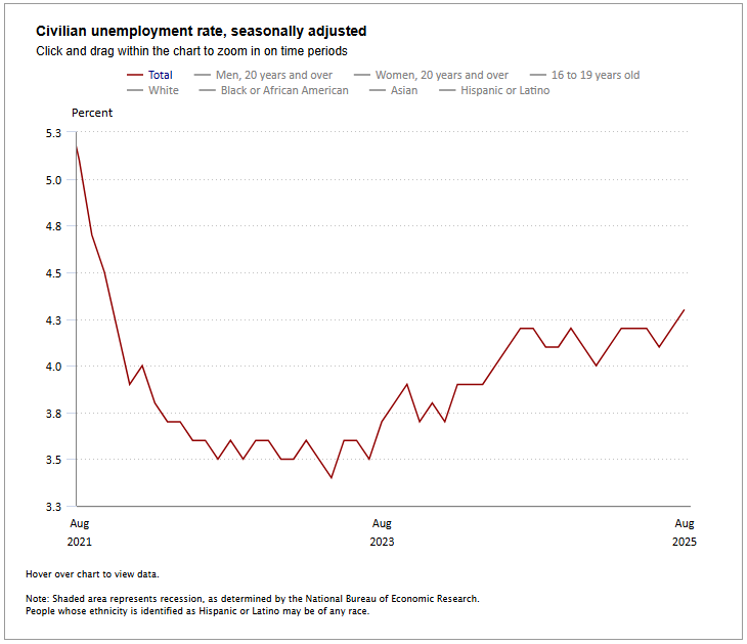

https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm

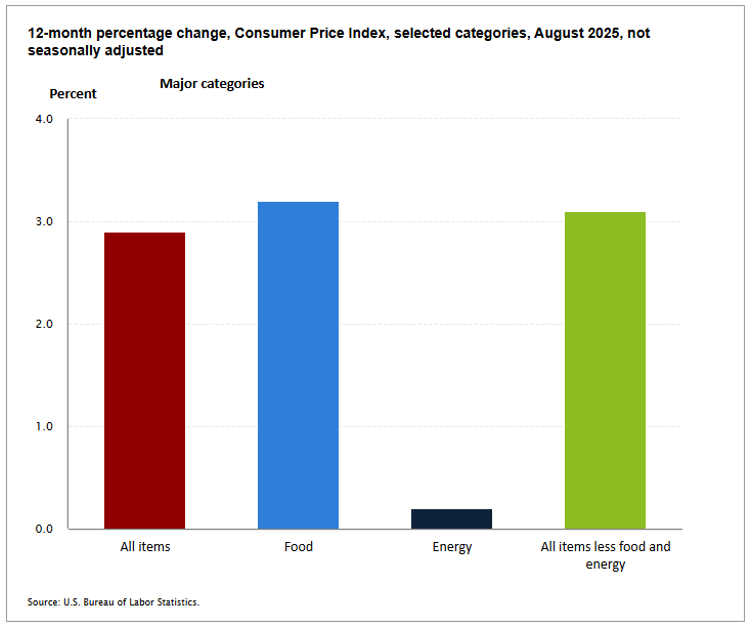

- Total non-farm payroll employment changed little in August (+22,000) and has shown little change since April, the U.S. Bureau of Labor Statistics (BLS) reported today.

- The unemployment rate, at 4.3 percent, also changed little in August. A job gain in health care was partially offset by losses in federal government and in mining, quarrying, and oil and gas extraction.

- This news release presents statistics from two monthly surveys.

- The household survey measures labor force status, including unemployment, by demographic characteristics.

- The establishment survey measures non-farm employment, hours, and earnings by industry.

Household Survey Data

- Both the unemployment rate, at 4.3 percent, and the number of unemployed people, at 7.4 million, changed little in August.

- The number of long-term unemployed (those jobless for 27 weeks or more) changed little at 1.9 million in August but has increased by 385,000 over the year. In August, the long-term unemployed accounted for 25.7 percent of all unemployed people.

- In August, the labor force participation rate changed little at 62.3 percent, and the employment-population ratio was unchanged at 59.6 percent. Both measures have declined by 0.4 percentage point over the year.

- The number of people not in the labor force who currently want a job, at 6.4 million, changed little in August but was up by 722,000 over the year. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

- The number of people employed part time for economic reasons, at 4.7 million, changed little in August. These individuals would have preferred full-time employment but were working part-time because their hours had been reduced or they were unable to find full-time jobs.

Establishment Survey Data

- Total non-farm payroll employment changed little in August (+22,000) and has shown little change since April. Over the month, a job gain in health care was partially offset by losses in federal government and in mining, quarrying, and oil and gas extraction.

- In August, health care added 31,000 jobs, below the average monthly gain of 42,000 over the prior 12 months. Employment continued to trend up over the month in ambulatory health care services (+13,000), nursing and residential care facilities (+9,000), and hospitals (+9,000).

- Employment in social assistance continued to trend up in August (+16,000), reflecting continued job growth in individual and family services (+16,000).

- Federal government employment continued to decline in August (-15,000) and is down by 97,000 since reaching a peak in January. (Employees on paid leave or receiving ongoing severance pay are counted as employed in the establishment survey.)

- Employment showed little change over the month in other major industries, including construction, retail trade, transportation and warehousing, information, financial activities, professional and business services, leisure and hospitality, and other services.

- Average hourly earnings for all employees on private nonfarm payrolls rose by 10 cents, or 0.3 percent, to $36.53 in August. Over the past 12 months, average hourly earnings have increased by 3.7 percent. In August, average hourly earnings of private-sector production and nonsupervisory employees rose by 12 cents, or 0.4 percent, to $31.46.

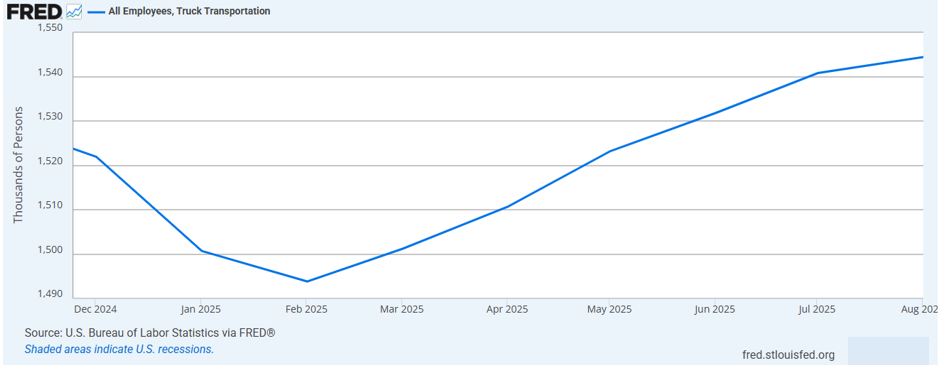

U.S. Truck Transportation Employment

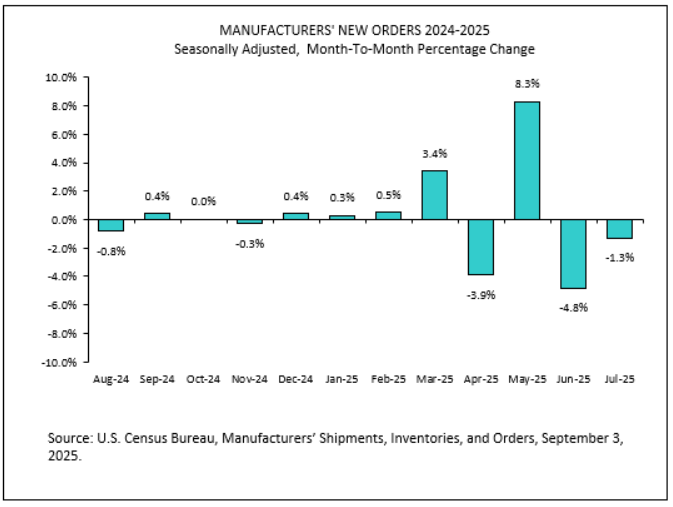

Manufactured Goods – New Orders

https://www.census.gov/manufacturing/m3/current/index.html

Monthly Full Report on Manufacturers’ Shipments, Inventories, & Orders

(Released September 3, 2025)

- New orders for manufactured goods in July, down three of the last four months, decreased $7.8 billion or 1.3 percent to $603.6 billion, the U.S. Census Bureau reported today. This followed a 4.8 percent June decrease.

- Shipments, up three consecutive months, increased $5.3 billion or 0.9 percent to $608.3 billion. This followed a 0.6 percent June increase.

- Unfilled orders, up twelve of the last thirteen months, increased $0.4 billion or virtually unchanged to $1,469.6 billion. This followed a 0.9 percent June increase.

- The unfilled orders-to-shipments ratio was 6.87, down from 7.01 in June. Inventories, up nine of the last ten months, increased $2.6 billion or 0.3 percent to $948.8 billion. This followed a 0.2 percent June increase.

Transportation Update

Fuel

https://www.eia.gov/petroleum/gasdiesel/?os=frefapp

The national average price of diesel for the week of August 25 stood at $3.71 per gallon, an decrease of 97 cents from four weeks prior at the end of July and up $0.057 from a year ago.

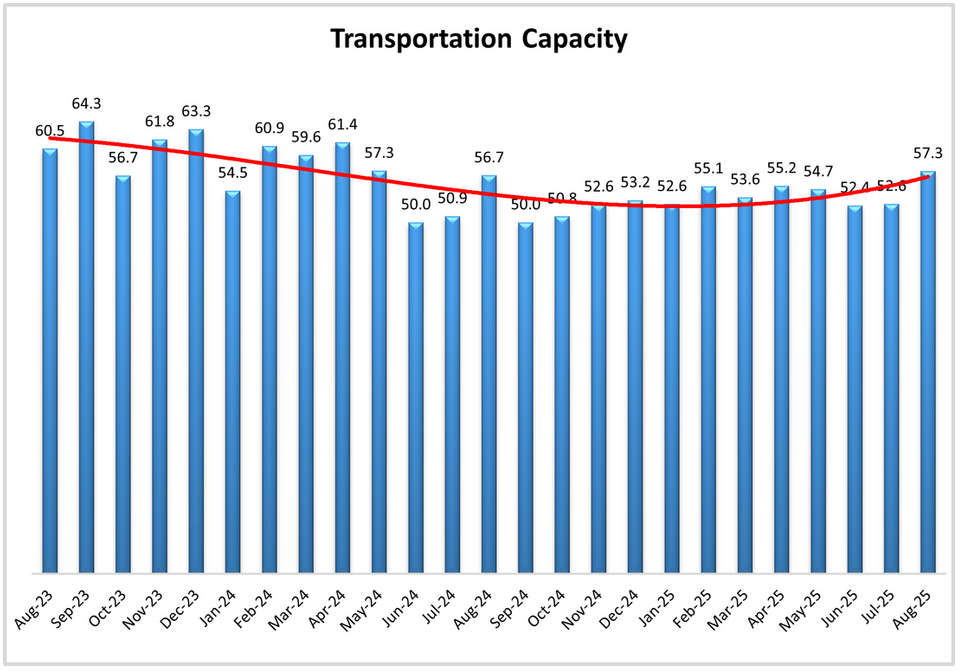

Transportation Capacity

- The Transportation Capacity Index increased 4.7 points to 57.3 percent in August 2025.

- Transportation Capacity index achieves a level not seen Since May of 2024, which marked the positive freight inversion than began the current cycle of expansion. It is therefore fitting that we hit this level again on the first month since then with a negative freight inversion.

- Transportation Capacity index is at 57.6, the Downstream index is slightly lower at 55.4 but the difference is not statistically significant.

- The future Transportation Capacity index moved back below the critical threshold, and it is now at 49.0,indicating slight contraction for the next 12 months. While the future Upstream index is at 48.5, the Downstream Transportation Capacity index is at 46.4, both indicating slight contraction, but the difference is not statistically significant.

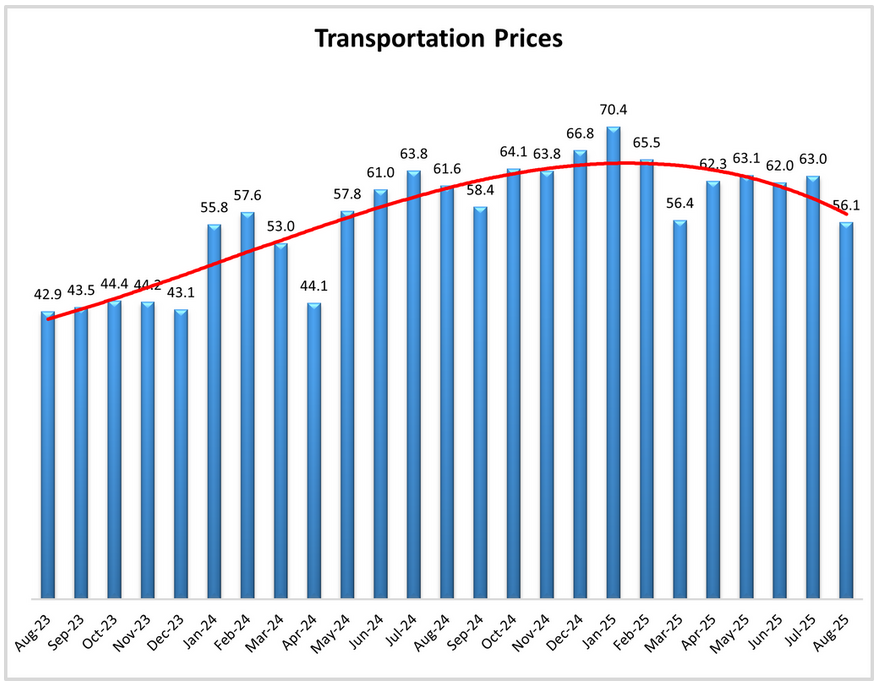

Transportation Prices

August 2025 Logistics Managers’ Index – LOGISTICS MANAGERS’ INDEX

- The Transportation Prices Index dropped 6.9 points from the previous reading and recorded 56.1 in August 2025. This is the lowest reading for this metric since April of 2024, which was the end of the 2022-2023 freight recession.

- This is driven by the Upstream Transportation Prices Index which is at 51.5, and the Downstream index is at 66.1 and the difference is statistically significant. As such, it can be concluded that the price increases that we see in transportation are felt stronger Downstream than Upstream.

- The future index for Transportation Prices also decreased from last month, indicating 3.6 points lower at 71.9. The Upstream future Transportation Prices index is at 72.8 while the Downstream Transportation Prices index is at 69.6, but the difference is not significant. As such, it can be concluded that expectations of higher Transportation Prices remain prevalent across the economy, both Upstream and Downstream supply chains.

Cass Freight & Truckload Index

Uncertainty Reigns

Source: Cass Information Systems, Inc.

Cass Transportation Index Report | August 2025 | Cass Information Systems

Cass Transportation Index Report | August 2025 | Cass Information Systems

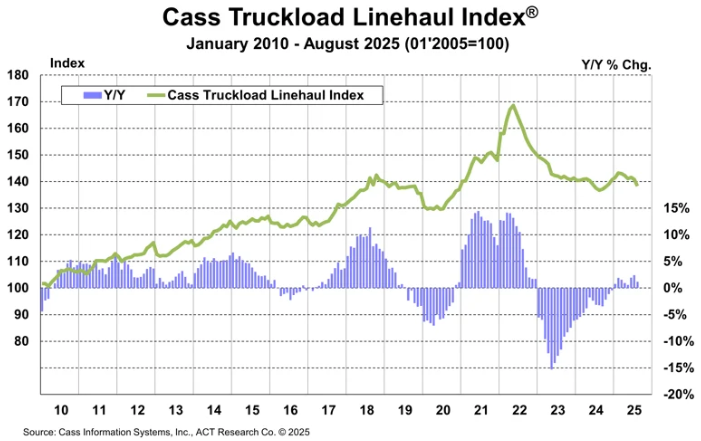

The Cass Truckload Linehaul Index is a measure of market fluctuations in per-mile truckload linehaul rates, independent of additional cost components such as fuel and accessorials.

The Cass Truckload Linehaul Index fell 1.8% m/m in August, after a 0.6% decrease in July.

- The y/y increase slowed to 1.2% in August from 2.4% in July.

- This index fell 10% in 2023, another 3.4% in 2024, and after a 1.3% increase in 1H’25, is on track for a small increase in 2025.

Truck Tonnage Index

ATA Truck Tonnage Index Rose 0.6% in July

From the American Trucking Associations (ATA) on August 19, 2025:

- In July, the ATA advanced seasonally adjusted For-Hire Truck Tonnage Index equaled 113.7, up from 113.0 in June. The index, which is based on 2015 as 100, slipped 0.1% from the same month last year after falling 0.4% in June. Year-to-date, compared with the same period in 2024, tonnage was unchanged.

- June’s SA decline was larger than first reported in our July 22 press release.

- The not seasonally adjusted index, which calculates raw changes in tonnage hauled, equaled 116.8 in July, 1.9% above June’s reading of 114.6.

- Trucking serves as a barometer of the U.S. economy, representing 72.7% of tonnage carried by all modes of domestic freight transportation, including manufactured and retail goods. Trucks hauled 11.27 billion tons of freight in 2024. Motor carriers collected $906 billion, or 76.9% of total revenue earned by all transport modes.

- Both indices are dominated by contract freight, as opposed to traditional spot market freight. The tonnage index is calculated on surveys from its membership and has been doing so since the 1970s. This is a preliminary figure and subject to change in the final report issued around the 5th day of each month. The report includes month-to-month and year-over-year results, relevant economic comparisons, and key financial indicators.

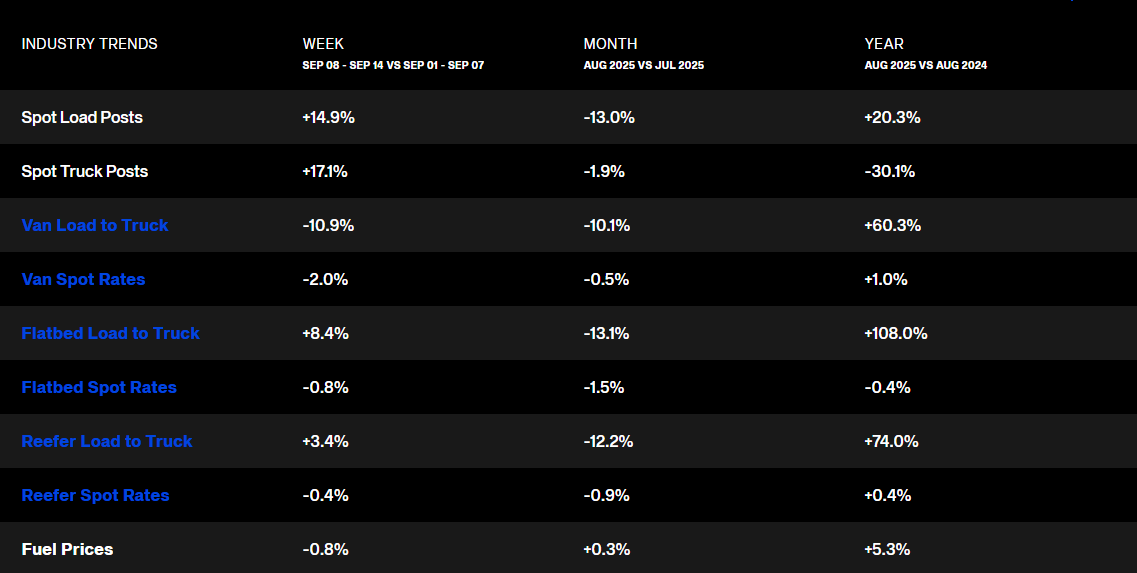

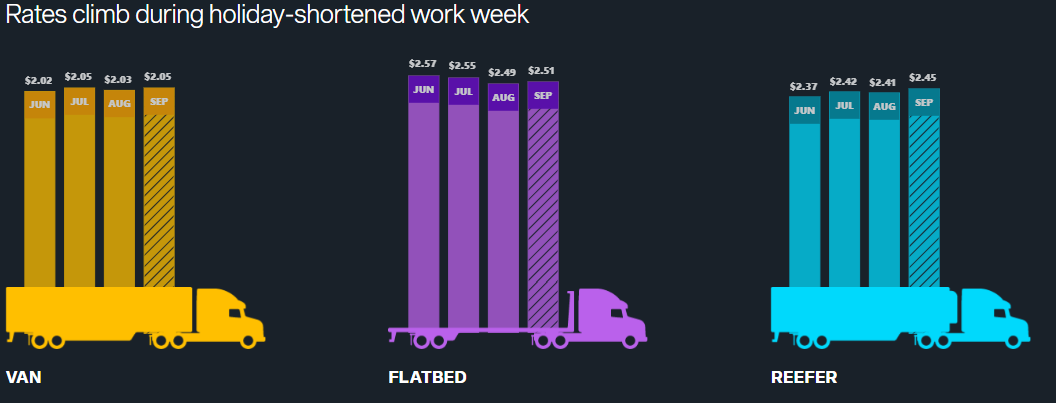

National Spot Rates

Source: DAT Analytics | https://www.dat.com/trendlines

The chart above depicts national average rates (including fuel surcharges) in the past 13 months, derived from DAT RateView.